Q1 Market Report 2026

Q1 Market Report 2026

After a challenging 2025 – defined by the combined pressures of US tariffs, geopolitical instability, and tighter fiscal conditions – the fine wine market entered 2026 facing a cautious and, at times, uncertain outlook. Pricing across key regions, particularly Bordeaux and Burgundy, remained under pressure for much of the year, while reduced liquidity and a more selective buyer base underscored a broader recalibration across the market.

However, as we move through the early months of 2026, there are emerging signs that the worst of this correction may be behind us. Leading indicators point towards a gradual improvement in sentiment: the broadest Bordeaux indices have now posted consecutive months of growth, suggesting that prices may have found the floor after a prolonged period of adjustment. At the same time, trading activity is beginning to pick up, with a steady increase in the number of active buyers re-engaging with the market.

This renewed participation is particularly notable. Throughout 2025, the market was characterised by caution, with many investors adopting a wait-and-see approach amid macroeconomic uncertainty and more attractive yields available in traditional financial instruments. The recent uptick in buyer numbers may therefore signal a shift in mindset, as relative value in fine wine becomes more compelling and confidence begins, albeit tentatively, to rebuild.

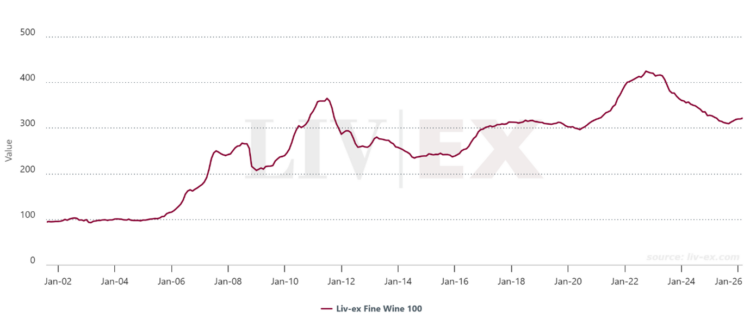

Figure 1 The Liv-ex Fine Wine 100 performance – this index tracks the price performance of 100 of the world’s most sought-after fine wines traded on the secondary market

What do the Liv-ex Stats Say?

The Fine Wine market continues to show encouraging signs of stability and selective growth. The Liv-ex 100, which tracks the 100 most sought-after fine wines on the secondary market, posted its sixth consecutive month of growth and is now up 3.9% since September 2025.

Trading activity in 2026 indicates strong buyer engagement, with 62% of trades in Q1 triggered by buyers – the highest level since Q1 2024. Trades are occurring closer to market price, now approximately 4% below, compared to 8% in August 2025. While February saw a slight easing in activity, with value down 4.1% and volume down 2.3% month-on-month, it remains the third-strongest month since the introduction of US tariffs in March 2025 and 20% above the Q2-Q3 2025 average.

Bordeaux remains dominant, accounting for 39% of traded volumes so far in 2026, with live bids on more than 8,500 bottles of First Growths – the highest since March 2022 – and is on track to record its highest quarterly share since Q2 2023. Overall, these trends suggest the market is consolidating, with strong underlying demand for top-end Bordeaux and other trophy wines creating selective investment opportunities.

By Edward Stevens – [email protected]